You don’t choose an electricity provider the way your grandparents did. You don’t choose a phone company the way your parents did. Within a decade, you won’t choose a bank the way you do now.

That sentence will make most people uncomfortable. Banks feel permanent. They feel structural. Your chequing account isn’t a subscription you cancel. It’s where your paycheque lands. It’s the routing number on your rent payment. It’s the debit card in your wallet. Switching banks feels like moving house. Which is exactly why most people don’t do it, even when they should.

But the relationship between a person and their financial products is about to be rearranged. Not by a new bank. Not by a better app. By a layer that sits above all of them and makes the question “which bank should I use?” as irrelevant as “which cell tower is carrying my call right now?”

This is a perspective on how that happens. What people believe today, what’s actually true, what behaviours already prove the shift is underway, and what conditions have to hold for the whole thing to work.

What people believe right now

The dominant mental model for personal finance is institutional loyalty. You have a bank. Maybe you inherited it from your parents. Maybe you opened an account at the university because there was a branch near campus. The relationship persists through inertia, not satisfaction.

This belief system has three layers.

The first is that your bank knows you. People assume their primary financial institution has a meaningful understanding of their financial life. It doesn’t. Your bank sees what passes through its own pipes. It sees your chequing balance, your mortgage payment, and your credit card transactions on its card. It does not see your Wealthsimple portfolio. It does not see your Amex spend. It does not see the HISA you opened at EQ Bank because the rate was three times better. Your bank has a partial view of your money and presents it as though it were the whole picture.

The second belief is that financial products belong together under one roof. That your mortgage, your chequing, your savings, your credit card, and your investments should all live at the same institution. Banks reinforce this aggressively through bundling discounts, loyalty programs, and the sheer friction of moving anything. The implicit message: it’s easier to stay. The unspoken truth: it’s more profitable for us when you do.

The third belief is that trust lives inside institutions. People trust RBC or TD or Scotiabank not because they’ve evaluated these companies’ risk management practices, but because the buildings are large, the logos are familiar, and the implicit government backstop (deposit insurance) makes failure feel impossible. This trust is real. It measures at 78% for banks versus 32% for third-party financial apps. But it’s institutional trust, not relational trust. People trust the building. They don’t trust the advice.

These three beliefs keep the current structure intact. They also happen to be increasingly wrong.

What’s actually happening

The supply side of personal finance is already modular. People just haven’t named it that way.

A typical financially engaged Canadian household in 2026 looks like this: chequing at one of the Big Five. A high-interest savings account at EQ Bank or Wealthsimple Cash, because the rate is materially better. A credit card from a different issuer, often Amex, chosen for rewards unrelated to the primary bank. Investments at a robo-advisor or self-directed brokerage. A mortgage from whichever lender won the rate negotiation at renewal time. Maybe a TFSA or RRSP parked somewhere else entirely.

This person already uses five or six financial providers. They already comparison-shopped their way into this arrangement. They already implicitly made the decision that no single institution deserves all of their business.

But the demand side hasn’t caught up. Every one of those relationships is managed separately. Separate logins. Separate apps. Separate statements. Separate customer service numbers. When a better savings rate appears, the person has to discover it, evaluate it, open a new account, verify their identity again, transfer the money manually, and remember to update their mental map of where everything sits. The cognitive and operational burden of managing a modular financial life falls entirely on the individual.

The banks benefit from this friction. Every inconvenience is a retention mechanism. The harder it is to leave, the fewer people leave. According to Accenture’s 2025 Global Banking Consumer Study, nearly three-quarters of banking customers globally have a relationship with at least one competing bank. The study’s conclusion was blunt: functional digital parity has pushed the industry into a state where every bank’s app is adequate, and no bank’s app is indispensable. The differentiation game on features is essentially over. Everyone is good enough. Nobody is great enough to justify consolidation.

Meanwhile, all five major Canadian banks are investing heavily in AI. RBC’s NOMI has delivered over two billion personalized insights and helped clients save $3.6 billion through automated savings features. TD is committed to generating C$1 billion annually in AI value and has 2,500 people working on it. Scotiabank’s AIDox system processes 90% of commercial client emails autonomously. BMO ranks number one globally in AI talent development. CIBC’s internal platform has saved over 600,000 hours since launch.

Every one of these investments points inward. The AI analyses the bank’s own data. The insights are about the bank’s own products. The recommendations lead to the bank’s own offerings. Not one of these banks has built anything that shows you a competitor’s product, even when the competitor’s product would serve you better. The walls are getting smarter, but they’re still walls.

Canada’s Consumer-Driven Banking Act, now progressing through Parliament, will change the plumbing. Phase 1, targeted for 2026, mandates API-based read access. Any accredited entity can pull a consumer’s financial data from multiple institutions with explicit consent. Phase 2, expected mid-2027, adds write access and payment initiation. That’s the moment when “switch my chequing to EQ” becomes something a system can execute, not just something a person can wish for.

What “open banking” actually means in practice

Banks don’t hand out passwords. But the effect is close. Under the Consumer-Driven Banking Act, every Schedule I bank in Canada will be legally required to build and maintain standardized APIs that let accredited third parties access customer data. The customer gives explicit consent. The bank provides the data. It can’t block it, slow-walk it, or make it painful.

What flows through those APIs in Phase 1: deposit account balances and transaction history; credit card balances, limits, and transactions; investment account holdings and activity; and loan details, including mortgages. Basically, everything a customer can see when they log into their own banking app. A third party, with permission, sees the same thing.

Phase 2 adds the ability to act. Initiate payments. Move money. Fund new accounts. Redirect direct deposits. Execute switching between institutions. Not just read the data. Write to it.

Not everyone can plug in. Third parties must be accredited through a regime overseen by the Bank of Canada and meet security standards, liability requirements, and consumer protection thresholds. Once the framework is operational, screen scraping gets banned entirely. The fragile, insecure workaround that current aggregators rely on disappears. Replaced by something regulated, standardized, and mandatory.

The UK built this seven years ago. It now has 13.3 million active users, 31 million payments monthly, and API availability averaging 99.88%. It works. The question in Canada is not whether the infrastructure functions. It’s who builds the intelligence on top of it.

The infrastructure companies are already in place.

Flinks, 80% owned by National Bank of Canada, provides connectivity to 15,000 North American institutions. Plaid, at a $6.1 billion valuation, has signed an API-based data access agreement with RBC covering its 14 million digital clients. SnapTrade offers something even further ahead: read-and-write access to investment accounts, enabling not just data retrieval but trade execution through APIs.

The AI companies are watching all of this closely. Anthropic launched Claude for Financial Services in July 2025, the most comprehensive dedicated financial vertical from any major AI company. It includes financial modelling tools and integrations with S&P Global, Moody’s, FactSet, and Morningstar. OpenAI took a different route: major bank partnerships rather than direct products. BBVA deployed ChatGPT Enterprise to all 120,000 employees across 25 countries. Santander rolled it out to 15,000.

Perhaps the most telling move: Block, Anthropic, and OpenAI co-founded the Agentic AI Foundation with the Linux Foundation, specifically to establish open standards for AI agents operating across financial systems. That’s infrastructure-level coordination for a future where AI agents autonomously manage money across institutions. Nobody builds standards for a future they don’t expect to arrive.

The pipes exist. The regulatory permission is arriving. The question is what sits on top.

The behaviours that prove this is coming

People don’t wait for permission to solve their own problems. They use duct tape. The duct tape is the evidence.

Wealthica, a Canadian platform, aggregates accounts from over 20,000 institutions into a single dashboard. It’s read-only. It can’t move money, can’t optimize, can’t recommend. It just shows you the picture. People use it anyway. The demand for “show me everything in one place” already exists. The product that satisfies it is crude. People accept the crudeness because the need is real.

Borrowell compares financial products from 50+ institutions and makes recommendations based on your credit profile. It earns referral fees from providers, which means its economic incentives aren’t fully aligned with yours. People use it anyway. They want someone, or something, to tell them what’s better. They’ll accept a conflicted intermediary rather than do the comparison themselves.

Rate-chasing behaviour is now mainstream. EQ Bank built a $10 billion deposit base largely on one proposition: a better interest rate than the Big Five. No branches. No relationship managers. Just a number that’s higher than the number at your current bank. Canadians opened accounts there not because they wanted a new bank, but because they wanted their idle cash to stop losing value. The behaviour is the signal: people will move money to a better product when the friction is low enough.

Wealthsimple’s trajectory is the clearest proof. Three million users. $100 billion in assets under administration. A $10 billion valuation. The company spans investing, trading, saving, spending, tax filing, and crypto. It acquired a Montreal AI research platform in August 2025. Its stated ambition is to integrate more of its clients’ financial lives under one roof. It even built a voice AI assistant that handles portfolio and transfer queries.

But Wealthsimple is itself a financial provider with products to sell. Its AI tools carry an explicit legal disclaimer: informational only, not personalized financial advice. It cannot be the neutral coordination layer because it has a structural conflict. It can’t serve you the best chequing account if the best chequing account is at EQ Bank, and Wealthsimple also offers chequing accounts. This is the same structural problem that limited every previous attempt at financial aggregation. The company that sells the products cannot also be the one that neutrally evaluates them.

The most telling recent development arrived in March 2026. Perplexity AI launched Perplexity Portfolio in partnership with Plaid, allowing users to connect brokerage accounts and ask natural-language questions about their holdings. It’s read-only. It covers only investments. It doesn’t touch banking, credit, mortgages, or insurance. But it’s the first major AI company to integrate directly with financial account data via open banking infrastructure. The pattern it establishes is clean: AI interface on top, financial data infrastructure below. The person asks a question in plain language. The system answers using their actual data.

That pattern will expand because consumers are already assembling a modular financial life and bearing the coordination costs alone. The behaviour precedes the product. Every person who manually moves money between a Big Five chequing account and an EQ Bank savings account, every person who checks Borrowell before opening a new credit card, every person who logs into Wealthica to see their full picture, is performing the job that the coordination layer will eventually automate.

What has to be true for this to work

Four conditions. All of them are hard. None of them are optional.

Trust has to transfer from institutions to the layer. This is the existential challenge. FCAC research found that only 9% of Canadians had heard of open banking. After being given a definition, only 15% said they’d participate. More than half said no. The protections people demanded were specific: full protection from financial losses, the ability to revoke consent at any time, mandatory breach reporting, and standard security requirements.

Trust in AI for financial services is even worse. A 2025 YouGov survey found just 19% of people trust AI in finance, while 48% actively distrust it. If an AI financial assistant makes a single mistake, 58% of consumers say they’d abandon it permanently.

There’s also what might be called the trust-under-stress problem. In calm markets, a pretty interface with smart suggestions can build a loyal user base. But stress exposes everything. A frozen account. A fraud incident. A market crash. A disputed charge. In those moments, people don’t ask, “Which app is smartest?” They ask, “Who stands behind my money?” The answer has to be clear and immediate. Wealthsimple’s own customer service data reveals that satisfaction collapses precisely in these moments. The complaints are consistent: accounts are frozen with no explanation, holds are placed with no escalation path, and automated responses are provided when a human is needed. If the coordination layer inherits those failure modes, it inherits the distrust that comes with them.

This isn’t a product problem. It’s a trust-market fit problem. The product can be flawless and still fail because people don’t believe it’s acting in their interest. The trust gap between banks (78%) and third-party apps (32%) suggests that the most viable path might be a layer embedded within or endorsed by a trusted institution, rather than a challenger brand starting from scratch. The UK’s emerging model, in which banks like HSBC display competitors’ accounts within their own AI-powered apps, may be the template.

The Synapse Financial Technologies bankruptcy provides the essential warning. At its peak, Synapse supported 18 million users and $9 billion in assets through banking-as-a-service partnerships. When it collapsed, $265 million in customer funds were frozen, and a shortfall of up to $96 million was identified. Customer money was effectively missing. Any coordination layer occupies the same structural position Synapse did. Powerful but fragile.

The business model has to prove alignment, not claim it. This is where most visions of the future get lazy. “We’ll recommend the best product for you” sounds great until you ask who pays for the recommendation. Every financial comparison site that has ever existed makes money by directing users toward providers who pay referral fees. Ratehub. NerdWallet. Borrowell. The user’s interest and the platform’s economic interest are not the same thing.

Three models can work. A subscription model where the user pays, and there are no referral economics. A clearly disclosed marketplace where referral fees are visible, and the user can see when a recommendation has economic incentives attached. Or an advisor-like retainer where the layer charges for the quality of guidance, the way a financial planner does.

The subscription model is the cleanest. It’s also the hardest to sell. People expect financial tools to be free. But the moment the layer routes users toward whoever pays the most instead of whoever serves them best, the core asset is gone. The core asset is belief. Belief that this thing is working for you, not extracting from you. Business model is a trust model. They’re the same thing.

The AI has to earn trust through accuracy, not claim it through promises. Financial AI cannot afford to be wrong. Not sometimes wrong. Not occasionally wrong. The tolerance for error in a system that touches your savings, your mortgage, and your retirement funds is effectively zero.

Origin Financial, the closest global analog to the full vision, runs a multi-agent architecture that passes every output through 100+ fiduciary compliance checks. It uses deterministic engines for math and LLMs only for scenario interpretation. This hybrid architecture, not pure AI, is the minimum viable approach. OSFI’s Guideline E-23, effective 2027, will formalize these requirements for federally regulated entities in Canada, including explainability and validation standards for AI models.

The accuracy bar is high. It should be. People’s financial lives aren’t test environments.

Liability has to be accepted, not avoided. This is the condition nobody wants to talk about. When a coordination layer acts on behalf of a user, moving money, switching accounts, redirecting payroll, someone has to be responsible if something goes wrong. Under Canada’s consumer-driven banking framework, liability allocation between data holders, data recipients, and service providers is a core design element.

The company that accepts meaningful liability for its recommendations sends a signal that no marketing claim can match. It’s saying: we believe in this enough to stand behind it financially. That acceptance of risk is a costly signal. It’s expensive to fake and impossible to copy cheaply. In positioning terms, it’s Gravity. It’s the structural decision that proves the position rather than claiming it.

Any company that builds the coordination layer but structures itself to avoid liability when things go wrong is telling you everything you need to know about how much it trusts its own product.

Where this ends up

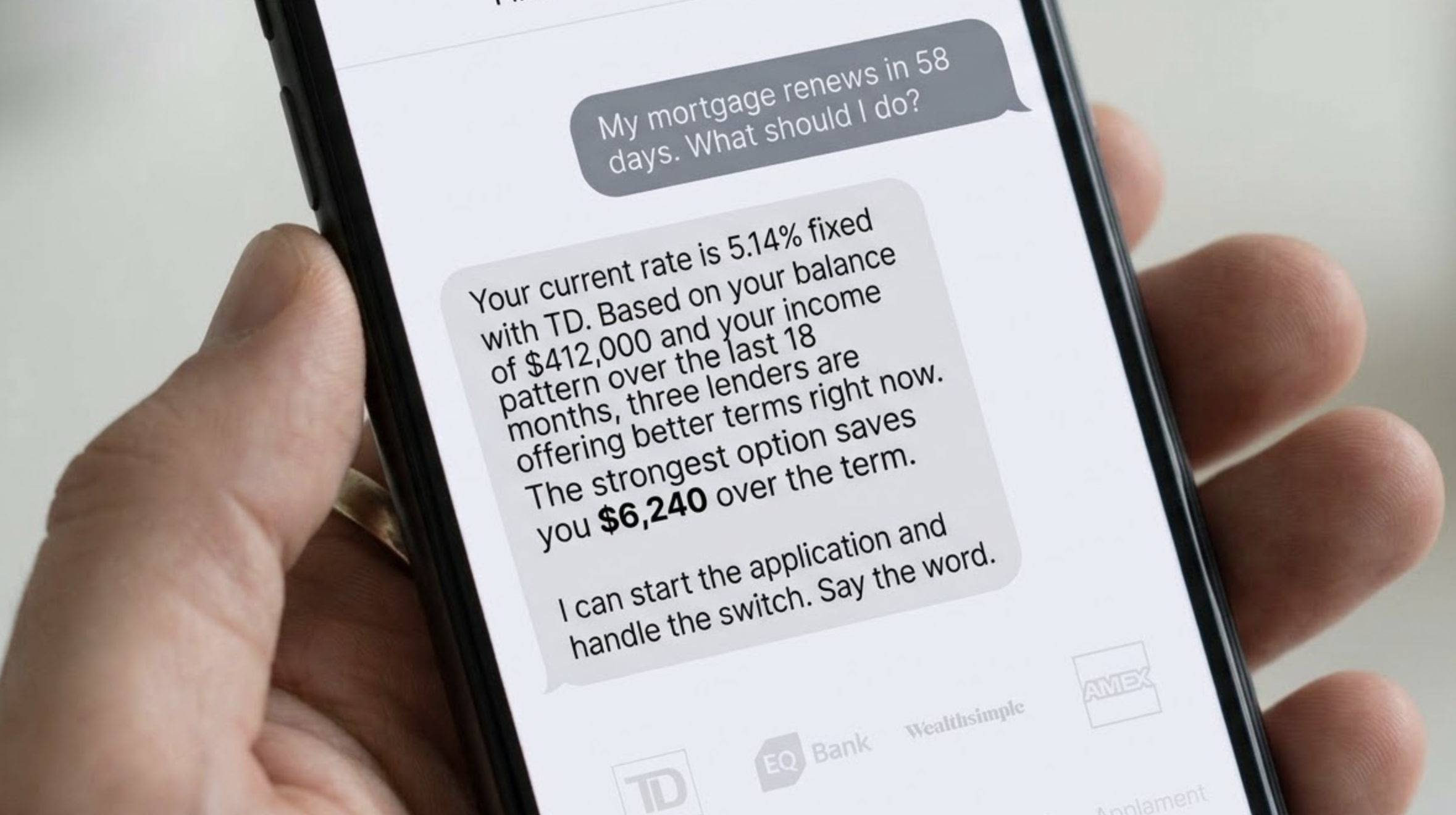

The person in this future doesn’t choose a bank. They don’t need to. They have one financial home. A single interface that sees everything, understands the full picture, and acts across providers on their behalf.

They say “my mortgage renews in two months, what should I do?” and get an answer grounded in their actual balance, their actual income, their actual risk tolerance, and the actual rates available from every lender in the market. Not a generic article about mortgage renewal. Not a comparison chart, they have to interpret themselves. A specific recommendation with the math shown.

They say, “Move my idle cash to whoever pays the best rate,” and it happens. No forms. No new login. No identity verification for the fourth time this year. The layer handles the complexity. The person handles the decision.

The banks still exist. They still hold deposits, issue mortgages, and underwrite risk. But they sit behind the layer, competing on product quality the way hotels compete on Booking.com or airlines compete on Google Flights. The relationship moves from the institution to the interface.

This is not a new pattern. It’s the oldest pattern in digital markets. When a better aggregation interface emerges, the underlying providers become infrastructure, whether they choose to or not. The airlines that invested in direct-booking technology retained more value than those that didn’t. The music labels that took equity in Spotify captured billions. The providers that fight the layer simply delay the inevitable while losing the opportunity to shape it.

The question for every player in Canadian financial services is not whether this coordination layer arrives. The behaviours already prove the demand. The infrastructure already exists. The regulation is on its way.

The question is whether you’ll be the interface or the infrastructure behind it. And whether the person managing their money will think of you as their financial home, or as a provider they barely remember the name of, somewhere behind the screen.

Addendum: The Five Prerequisites — Where They Actually Stand

In the original piece, I identified four conditions for the coordination layer to work: trust transfer, business model alignment, AI accuracy, and liability acceptance. Those are market conditions; they test whether consumers and builders can make the thing succeed. This addendum examines the five regulatory and infrastructure prerequisites that must be in place before any of those four conditions can even be tested. If these five aren’t met, nothing else matters.

1. The law has to exist and pass

The Consumer-Driven Banking Act is Division 9 of Bill C-15, the Budget 2025 Implementation Act, tabled November 18, 2025. It establishes the full legal architecture: a mandatory data-sharing framework where consumers direct their financial data to participating entities of their choice; an accreditation regime for third parties overseen by the Bank of Canada; liability allocation between data holders, data recipients, and service providers; security safeguards, consent management, and authentication standards; and the explicit prohibition of screen scraping once the framework is operational.

Bill C-15 passed third reading in the House of Commons on February 26, 2026. It was referred to the Standing Senate Committee on National Finance on March 10, 2026, and Senate committee hearings are actively underway. Royal Assent has not yet been granted.

This is not a concept paper or a consultation. The legislative text is written. It has cleared the House. What remains is Senate committee review, third reading in the Senate, and Royal Assent. The substance of the CDBA has not been contentious in parliamentary debate; the bill is an omnibus budget implementation act moving on a government-priority timeline. But it is not law yet, and the downstream implementation sequence (regulations, accreditation, API standards) cannot formally begin until it is.

Status: Passed the House of Commons. In Senate committee as of March 10, 2026. Royal Assent pending. Implementation work (regulations, accreditation framework, API standards) follows.

2. The data pipes have to be open and standardized

Phase 1 of the CDBA mandates standardized, API-based read access. Any accredited entity will be able to pull a consumer’s deposit balances, transaction history, credit card data, investment holdings, and loan details (including mortgages) from any Schedule I bank, with the consumer’s explicit consent.

The government’s stated target has been to launch the open banking framework in 2026. Given that the CDBA is still before the Senate and supporting regulations have not yet been finalized, the 2026 target for functioning Phase 1 read access is under pressure. The accreditation process must be operationalized, API standards must be published, and banks must build or formalize their API infrastructure to comply. None of this can formally begin until Royal Assent.

The infrastructure providers who will connect to these APIs already exist and are operational today. Flinks has connectivity to 15,000 North American institutions and is majority-owned by National Bank. Plaid has a formal API data access agreement with RBC covering its 14 million digital clients. SnapTrade offers read-and-write access to investment accounts. The data connectivity problem is substantially solved by existing aggregators that use consent-based access. What the CDBA adds is not the ability to connect (which already exists) but a legal mandate that banks cannot block, throttle, or degrade access. The shift is from permission-based to rights-based.

Phase 2 adds write access: payment initiation, account funding, direct deposit redirection, and product switching. The expected timeline is around 2027, contingent on both the regulatory framework being operational and the Real-Time Rail being live.

Status: CDBA awaiting Royal Assent. Phase 1 read access is targeted for 2026, but the timeline is tight given legislative status. Phase 2 write access is expected around 2027. Existing aggregator infrastructure already covers most major FIs today.

3. Money has to move in real time

Phase 2 of the CDBA (write access and payment initiation) depends on a functioning real-time payment rail. Without it, automated money movement remains batch-processed, slow, and operationally limited. Canada’s Real-Time Rail is being built by Payments Canada with delivery partners IBM Canada and CGI, and exchange infrastructure from Interac.

The RTR completed system integration testing on schedule in Q4 2025, during which all individual components were integrated and tested as a single system. In Q1 2026, the program entered user acceptance testing — testing at peak volumes to ensure the system can handle high-volume transactions in real time. Payments Canada is targeting a Q3 2026 launch, with broader industry testing and onboarding running in parallel through 2026 and into 2027.

Honesty requires noting the history. RTR planning began in 2019. The program was paused entirely in 2023 for reassessment. It resumed in April 2024 with new delivery partners and renewed timelines. Payments Canada has adjusted projected timelines multiple times before. The current phase is the furthest the program has ever advanced, and the momentum is qualitatively different from prior cycles. The technical build is complete, integration testing is complete, and new PSP members are actively being onboarded. But a history of delays warrants measured confidence rather than certainty.

The RTR is designed for 24/7/365 instant clearing and settlement with ISO 20022 data richness. When it is live and at scale, a coordination layer can execute real-money movement (sweep idle cash to the best rate, fund new accounts at competing institutions, initiate payments, and redirect direct deposits) programmatically and instantly.

Status: Technical build complete. User acceptance testing underway as of Q1 2026. Q3 2026 launch targeted. Broader industry rollout through 2026–2027. The current phase is the most advanced in program history, but prior delays warrant caution.

4. Non-banks have to be allowed into the payment system

This is the prerequisite most people overlook, and the one that has made the most concrete progress. It is not enough for the data pipes to be open. The entities building on top of those pipes need direct access to the core payment clearing and settlement systems. Without that access, every transaction still routes through a bank, and the bank retains a chokepoint.

Two things happened in sequence that changed this.

First, the Retail Payment Activities Act came fully into force on September 8, 2025. PSPs who registered with the Bank of Canada during the November 2024 application window are now supervised entities with clear obligations around safeguarding funds, operational risk management, and incident reporting. The Bank of Canada’s PSP registry is live and operational.

Second, amendments to the Canadian Payments Act expanded membership eligibility to include PSPs registered under the RPAA, credit union locals, and designated clearing house operators. For the first time, non-bank fintechs can apply for direct membership in Payments Canada and, once members, begin the formal process to participate directly in national payment systems, including the RTR.

In January 2026, the first five PSPs were admitted as Payments Canada members: Wise, Float Financial, KOHO, Paramount Commerce (Element Financial Technology), and Brim Financial. These are not pilot participants or advisory members. They are full members with the ability to shape governance, participate in policy, and apply to connect directly to the RTR once it is live.

This closes the loop. The CDBA gives data access rights. The RTR provides instant payment capability. The Canadian Payments Act amendments and the RPAA give non-bank entities the legal standing and system access to use both. A coordination layer built by an AI-first actor would enter this system not as an outsider requesting access from banks, but as an accredited, supervised, directly-connected participant in Canada’s national payment infrastructure.

Status: RPAA fully in force since September 2025. Bank of Canada PSP registry operational. Payments Canada membership expanded. First five non-bank PSPs admitted January 2026. Direct RTR participation pathway established. This is the most advanced of the five prerequisites.

5. AI governance has to have clear, published rules

The coordination layer I described in the original piece is, at its core, an AI system making financial recommendations and executing actions on behalf of consumers. Regulators will not tolerate a black box sitting between Canadians and their money. The rules for how AI models must be governed in financial services need to be explicit, published, and enforceable.

OSFI’s Guideline E-23 on Model Risk Management was published September 11, 2025, and takes effect May 1, 2027 for all federally regulated financial institutions — banks, foreign bank branches, insurance companies, trust and loan companies. It establishes a comprehensive framework: institutions must maintain enterprise-wide model inventories; every model must be risk-rated using quantitative and qualitative criteria including complexity, level of autonomy, customer impact, and regulatory risk; governance intensity must be proportional to the model’s risk rating; and explainability requirements are explicit — the outputs of models must be interpretable and communicable to appropriate stakeholders.

Critically, E-23 extends to third-party models and vendors. Any coordination layer that plugs into a federally regulated institution’s systems (which is exactly what the CDBA enables) will be subject to these standards either directly or through the institution’s vendor oversight obligations. This means the AI governance bar is not optional for a serious builder. It is a condition of access.

This is good news for a willing actor, not a barrier. E-23 does not say “don’t use AI in finance.” It says, “Here is exactly how you must govern AI in financial services.” It converts regulatory uncertainty, which kills investment, into regulatory clarity, which enables it. A builder who designs their architecture to be E-23 compliant from day one has a durable advantage over anyone who builds fast and tries to retrofit compliance later.

Status: Guideline published September 2025. Effective May 1, 2027. FRFIs and their third-party vendors are in active preparation. The compliance framework is written, dated, and unambiguous.

What this means for a willing actor

The five prerequisites are at different stages of maturity, but all of them are either in force, in final testing, or on dated timelines:

- Non-bank system access (Condition 4): Live. RPAA in force. PSP members admitted. This is ready now.

- AI governance (Condition 5): Published. Effective May 1, 2027. The playbook exists. Preparation is underway.

- Real-time payments (Condition 3): In final testing. Q3 2026 launch targeted. The furthest RTR has ever advanced, though history warrants caution.

- Data access law (Condition 1): Passed the House. In the Senate committee. Royal Assent pending. Not yet law, but the legislative text is written and moving.

- Standardized data pipes (Condition 2): Dependent on Condition 1. Phase 1 read access targeted for 2026 but under timeline pressure. Existing aggregators bridge the gap in the interim.

The practical sequence for a builder looks like this:

- Now (Q1 2026): Begin architecture and accreditation planning. Pursue RPAA registration and Payments Canada membership. Design for E-23 compliance. Build on existing aggregator infrastructure for read-only data access.

- Mid-to-late 2026: If the CDBA receives Royal Assent and Phase 1 regulations are finalized, transition from aggregator-based access to standardized API access. If RTR launches on schedule, begin integrating real-time payment capabilities.

- 2027: Phase 2 write access comes online. E-23 takes effect. The coordination layer gains the ability to act — move money, switch products, initiate payments — under a clear governance and liability framework.

No single prerequisite is speculative. Each one has a legislative text, a published guideline, a testing milestone, or an operational date attached to it. The regulatory and infrastructure environment in Canada is converging on a specific window, roughly 2026 through 2027, during which all five prerequisites reach operational maturity within months of one another.

Whether someone builds the coordination layer that sits on top of this stack is an execution question. Whether the stack itself will exist is no longer in question. It is being assembled now.

Leave a Reply

You must be logged in to post a comment.